Vancouver, B.C. August 14, 2017 – GLG Life Tech Corporation (TSX: GLG) (“GLG” or the “Company”), a global and agricultural leader in the natural zero-calorie sweetener industry, committed to the sustainable development of high-quality zero-calorie natural sweeteners, announces financial results for the three and six months ended June 30, 2017. The complete set of financial statements and management discussion and analysis are available on SEDAR and on the Company’s website at www.glglifetech.com.

FINANCIAL HIGHLIGHTS

- Six-month international stevia sales volumes doubled year-over-year

- Six-month international stevia sales increased 74% year-over-year

- Six-month gross profit margin improved by 8 percentage points year-over-year

- Six-month SG&A expenses cut by 21% year-over-year

- Debt reduced by $15.9 million following shareholder approval of first phase of $100 million debt restructure proposal

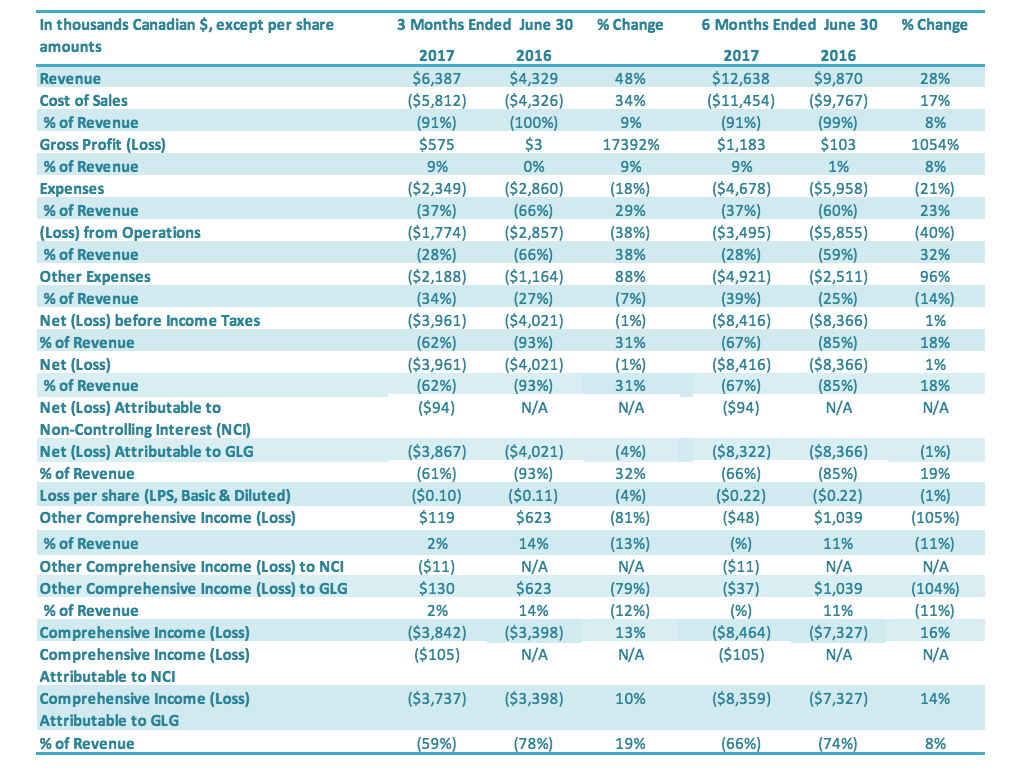

International stevia sales volumes again doubled in the second quarter 2017, year-over-year, continuing the trend from first quarter 2017. This trend reflects the increasing demand for GLG’s stevia extracts, resulting from the positive impact of GLG’s global distributorship agreement and its distributor’s success in the marketplace. International stevia revenues rose to $5.8 million, up 55% from $3.7 million. The Company had previously forecast strong growth in its international stevia sales, based on the strength of its product portfolio and product demand from its global distributor. Revenue for the three months ended June 30, 2017, was $6.4 million compared to $4.3 million in revenue for the same period last year, an increase of 48%. Six-month revenue was $12.6 million compared to $9.9 million for the same period last year, up 28%. The revenue increase was driven by the two-fold increase in international stevia sales volumes, which was partly offset by a decrease in monk fruit sales. International sales continue to be the dominant component of consolidated revenues, at 93% in the second quarter of 2017 (compared to 92% for the comparable period in 2016) – a result of both the Company’s continued focus on higher-purity stevia extract sales internationally and a decline in lowerpurity extract sales in China. Gross profit and gross profit margins both improved significantly in for the three and six months ended June 30, 2017. For the second quarter, gross profit was $0.6 million and gross profit margin was 9%, compared to nil gross profit/margin for the same period last year. The increase in gross profit for the second quarter of 2017, relative to the comparable period in 2016, is attributable to: (1) a 55% increase in international stevia sales and (2) decreased idle capacity charges in the second quarter of 2017 compared to the same quarter of 2016. Similarly, for the first six months of 2017, a 74% increase in international stevia sales and decreased idle capacity charges contributed to significant improvements in gross profit and gross profit margins, with gross profit at $1.2 million, compared to $0.1 million for the comparable period in 2016, and gross profit margin at 9%, compared to 1% for the comparable period. The Company continues to be successful in reducing its SG&A expenses, having reduced these expenses by 18% year-over-year in the second quarter of 2017 and by 21% year-over-year for the first six months of 2017 (each relative to the comparable period in 2016). This improvement results from the Company’s continued focus on tight cost controls on administrative expenses while simultaneously growing its revenues. Net loss for both the three and six month periods ending June 30, 2017, improved by $0.1 million yearover-year. The second quarter net loss was $3.9 million compared to a $4.0 million net loss in second quarter 2016, and the six month net loss was $8.3 million compared to an $8.4 million net loss for the first six months of 2016. During the second quarter, the Company achieved a major milestone in its debt restructuring efforts. At the Company’s Annual General and Special Meeting (the “Meeting”), held on May 29, 2017, the shareholders overwhelmingly approved the first phase of a two-phase debt restructuring plan. The first phase was a related party transaction (the “Transaction”) eliminating Company’s related party Chinese debt held by the Company’s Chairman and CEO and family members; in exchange, the related parties received minority equity ownership in GLG’s primary Chinese subsidiary (the “Subsidiary”). The Company has since fully executed the Transaction. As a result, it has removed $15.9 million in debt liability from its balance sheet. Completing this Transaction was not only important for reducing the Company’s related party debt; more significantly, it is a prerequisite of the Chinese bank debtholders to proceed with the second phase of the debt restructuring plan. The second phase involves restructuring the debt owed to the China-based lenders; under the phase two proposal, their debt holdings of $64.4 million, along with accrued interest and penalties of $19.6 million, will be eliminated in exchange for a proposed 25% stake in equity ownership in the Subsidiary. Together, once the second phase is agreed to by all parties and completed, the restructuring plan will have eliminated approximately $80 million in debt principal, have waived approximately $20 million in accrued interest and penalties, and save approximately $8 million in annual interest expenses. The Company expects to retain over 50% ownership and management control of the Subsidiary after these two phases of debt restructure are complete. The Company aims to complete this second phase in Q3 or Q4 2017.

Outlook

We continue to expect significant growth in our international stevia sales in 2017, driven by our partnership with our global distributor. Considering our distributor’s size and distribution reach, we expect that the partnership will continue to deliver significantly higher sales to GLG. Our international stevia revenues have increased significantly for the six months ended June 30, 2016, up 74% over the same period in 2016, and our international stevia volumes have doubled compared to that same period. As our global distributor leverages its existing customer relationships, distribution channels, and ingredient expertise in the food and beverage space, we expect international stevia revenues to continue to grow. We see significant sales opportunities arising from this partnership. Moreover, the partnership presents opportunities to develop and deliver new stevia products that have not historically been part of our portfolio. Between new products, immediate product demand from our distribution partner, and the global sales potential to supply many more customers worldwide, we expect to see continued growth in the next twelve months. We also continue to see sales opportunities for our monk fruit business. We believe that our ClearTaste Monk Fruit product line offers the best tasting monk fruit extract in the market today. This unique product removes citrus and astringent notes that otherwise complicate product formulators’ efforts to use monk fruit as a prime sweetener. We have received a lot of positive feedback from a variety of customers who prefer ClearTaste Monk Fruit over regular monk fruit extracts. We now have a pipeline of customers who are actively trialing this product, including some who have begun ordering our ClearTaste Monk Fruit products. However, despite the sales opportunities, we believe that the value of the monk fruit extract market has declined significantly from 2015/2016 due to lower pricing and lower volumes used in the food, beverage and supplement industry. Notwithstanding this year’s lower prices, the main driver of this industry decline in monk fruit volumes is the relatively high price of monk fruit compared to stevia. There are new solutions available in the market to make stevia taste better that offer lower cost in use than the use of monk fruit extract or blends of stevia and monk fruit. One of those solutions that GLG offers is ClearTaste Stevia. In addition, GLG is succeeding with its own direct sales efforts in the dietary supplement market, distinct from the food and beverage space covered by our distribution partnership. We have been successfully landing new accounts in this market for both stevia and monk fruit products. This new business stream began placing orders starting in the fourth quarter of 2016 and we continue to expect significant growth in the dietary supplement sector. We continue to grow the number of customers interested in ClearTaste Stevia, and have successfully added a number of new customers in the first six months of 2017, with a growing pipeline of prospective customers, and we expect to convert a percentage of these into paying customers. Our ClearTaste Stevia products provide better tasting stevia extracts that remove a number of the taste issues typically associated with stevia extracts, including bitter and astringent notes. With respect to our Naturals+ product line, we expect to develop sales with new/differentiated products such as our P-Pro Plus product as well as select natural ingredients that our customer base is currently sourcing. Finally, the Company has developed a two-phase plan designed to eliminate approximately $100 million in outstanding debt and interest, with the first phase subject to shareholder approval. The first phase was completed after the Shareholder Meeting held on May 29, 2017 (see the Related Party Debt Conversion section in the MD&A for details). The Company then expects to finalize the second phase in the fourth quarter of 2017. Please see the Financial Highlights section above and our Management Proxy Circular, available on SEDAR and on the Company’s website (www.glglifetech.com), for further details.

Corporate and Sales Developments

GLG Announces Debt Restructuring Shareholder Approval of its Debt Restructuring Proposal The Company held its Annual General and Special Meeting (the “Meeting”) on May 29, 2017, in Richmond, British Columbia, at which shareholders were asked to vote on a major step in the Company’s debt restructuring plans. The Company’s Board of Directors had appointed an Independent Special Committee to oversee the debt restructuring process, which led to a two-phase plan to eliminate over 80% of the Company’s outstanding debt and interest. The process the Board utilized in developing its recommendation to shareholders for the restructuring of its China-based debt is described in the Meeting Circular. As part of the Special Shareholder Meeting, shareholders were asked to vote on the first phase of this two-phase plan. The first phase is a related party transaction (the “Transaction”) to eliminate the Company’s related party Chinese debt held by the Company’s Chairman and CEO and family members; in exchange, the related parties receive minority equity ownership in GLG’s primary Chinese subsidiary (the “Subsidiary”). As a related party transaction, under TSX rules, the Company was required to obtain majority shareholder approval from disinterested shareholders. On May 29, 2017, the Company reported that the shareholders had approved the Transaction. Of the eligible votes cast, 18,037,225 eligible voting shares, representing 99.64% of the eligible votes cast, voted in favor of the Transaction. The Company has since fully executed the Transaction. Completing this Transaction was not only important for reducing the Company’s related party debt; more significantly, it is a prerequisite of the Chinese bank debtholders to proceed with the second phase of the debt restructuring plan. As President and CFO Brian Meadows commented after the meeting: “We are pleased to have the required approval to complete this first phase of our debt restructuring plan. We will now turn our attention to completing the second phase, whereby we expect to eliminate the substantial debts held by Chinese banks and state-owned capital management companies. As our Board’s Independent Special Committee concluded, we view this restructuring plan as very beneficial for our shareholders and for our Company’s plans for growth.” The second phase involves restructuring the debt owed to the China-based lenders; under the proposal, their debt holdings of $64.4 million, along with accrued interest and penalties of $19.6 million, will be eliminated in exchange for a proposed 25% stake in equity ownership in the Subsidiary. Together, once the second phase is agreed to by all parties and completed, the restructuring plan will have eliminated approximately $80 million in debt principal, have waived approximately $20 million in accrued interest and penalties, and save approximately $8 million in annual interest expenses. The Company expects to retain over 50% ownership and management control of the Subsidiary after these two phases of debt restructure are complete. The Company aims to complete this second phase in Q3 or Q4 2017. Such substantial reduction in debt will greatly improve the Company’s balance sheet and its ability to generate new sources of working capital to fund sales expansion. GLG Announces Re-Election of Board of Directors Concurrent with the May 29, 2017, transaction approval announcement, the Company also announced that the shareholders voted in all nominated directors, with favorable votes for each exceeding 99.9%. Dr. Luke Zhang continues as Chairman of the Board and Chief Executive Officer and Brian Palmieri continues as Vice Chairman of the Board.

SELECTED FINANCIALS

As noted above, the complete set of financial statements and management discussion and analysis for the three and six months ended June 30, 2017, are available on SEDAR and on the Company’s website at www.glglifetech.com.

Results from Operations

The following results from operations have been derived from and should be read in conjunction with the Company’s annual consolidated financial statements for 2016 and the condensed interim consolidated financial statements for the six-month period ended June 30, 2017.

Revenue

Revenue for the three months ended June 30, 2017, was $6.4 million compared to $4.3 million in revenue for the same period last year, an increase of 48%. International stevia sales volumes doubled over the same period in the previous year. This result continues to show the positive impact of GLG’s global stevia distribution partner’s success in the marketplace. Sales revenue for international stevia rose to $5.8 million in the second quarter compared to $3.7 million in the prior period or an increase of 55%. Sales increases reflected continued growth in both sales to new customers and sales of new products to existing customers. International stevia sales represented 93% of all stevia sales. Offsetting the increased international stevia sales was lower monk fruit sales, which decreased for the quarter by 57% over the same period last year. The decrease in monk fruit sales reflects lower prices for monk fruit extracts (a 7% lower average sales price compared to the second quarter in 2016). The volumes for monk fruit in the second quarter were also lower compared to the second quarter 2016. Our expectation is that there is a lower volume of monk fruit being purchased generally in the market compared to the previous two years. Even with lower market pricing, the cost of monk fruit extract is significantly higher – approximately 250% higher – than stevia. Revenue for the six months ended June 30, 2017, was $12.6 million, an increase of 28% compared to $9.9 million in revenue for the same period last year. International stevia sales volumes doubled over the same six-month period in the previous year. This result continues to show the positive impact of GLG’s global stevia distribution partner’s success in the marketplace. Sales revenue for international stevia rose to $11.1 million for the first six months in 2017 compared to $6.3 million in the same prior year period or an increase of 74%. Sales increases reflected continued growth in both sales to new customers and sales of new products to existing customers. International sales accounted for 93% of total sales in the first six months of 2017 compared to 88% in the comparable period of 2016. Offsetting the increased international stevia sales was lower monk fruit sales which decreased for the six month period by 72% over the same period last year. The decrease in monk fruit sales reflects significantly lower prices for monk fruit extracts (a 7% lower average sales price compared to the six months in 2016). The volumes for monk fruit in the six month period in 2017 were also lower by 70% compared to the six months in 2016. Our expectation is that there is a lower volume of monk fruit being purchased generally in the market compared to the previous two years. Even with lower market pricing, the cost of monk fruit extract is significantly higher – approximately 250% higher – than stevia.

Cost of Sales

For the quarter ended June 30, 2017, the cost of sales was $5.8 million compared to $4.3 million in cost of sales for the same period last year (an increase of $1.5 million or 34%). Cost of sales as a percentage of revenues was 91% for the second quarter 2017, compared to 100% for the comparable period (an improvement of 9 percentage points). Cost of sales as a percentage of revenues for the second quarter, relative to the same period in 2016, improved significantly for monk fruit; idle capacity charges were also lower for the quarter compared to the prior period. For the six months ended June 30, 2017, the cost of sales was $11.5 million compared to $9.8 million for the same period of last year (an increase of $1.7 million or 17%). Cost of sales as a percentage of revenues was 91% for the first six months 2017, compared to 99% in the comparable period in 2016 (an improvement of 8% percentage points). The 8 percentage point improvement in cost of sales as a percentage of revenues for the first six months of the year, relative to the same period in 2016, was driven by two factors: (1) a significant decrease in the cost of monk fruit extract and (2) lower idle capacity charges (a 32% improvement). Capacity charges charged to the cost of sales ordinarily would flow to inventory and are a significant component of the cost of sales. Only two of GLG’s manufacturing facilities were operating during the first six months of 2017, and idle capacity charges of $1.0 million were charged to cost of sales (representing 9% of cost of sales) compared to $1.5 million charged to cost of sales in same period of 2016 (representing 16% of cost of sales). The key factors that impact stevia and monk fruit cost of sales and gross profit percentages in each period include:

- Capacity utilization of stevia and monk fruit manufacturing plants.

- The price paid for stevia leaf and monk fruit and their respective quality, which are impacted by crop quality for a particular year/period and the price per kilogram for which the stevia and monk fruit extracts are sold. These are the most important factors impacting the gross profit of GLG’s stevia and monk fruit business.

- Other factors which also impact stevia and monk fruit cost of sales to a lesser degree include:

- water and power consumption;

- manufacturing overhead used in the production of stevia and monk fruit extract, including supplies, power and water;

- net VAT paid on export sales;

- exchange rate changes; and

- depreciation

GLG’s stevia and monk fruit businesses are affected by seasonality. The harvest of the stevia leaves typically occurs starting at the end of July and continues through the fall of each year. The monk fruit harvest takes place typically from October to December each year. GLG’s operations in China are also impacted by Chinese New Year celebrations, which occur approximately late-January to mid-February each year, and during which many businesses close down operations for approximately two weeks. GLG’s production year runs October 1 through September 30 each year.

Gross Profit

Gross profit for the three months ended June 30, 2017, was $0.6 million, compared to nil for the comparable period in 2016. The gross profit margin was 9% in the second quarter 2017 and 0% for the same period in 2016. The increase in gross profit for the second quarter of 2017, relative to the comparable period in 2016, is attributable to: (1) a 55% increase in international stevia sales and (2) decreased idle capacity charges in the second quarter of 2017 compared to the same quarter of 2016. Gross profit for the first six months in 2017 was $1.2 million, compared to $0.1 million for the comparable period in 2016 or a 1000% increase. The increase in gross profit for the six months ended June 30, 2017, relative to the comparable period in 2016, is attributable to: (1) a 74% increase in international stevia sales and (2) decreased idle capacity charges in the second quarter of 2017 compared to the same quarter of 2016.

Selling, General, and Administration Expenses

Selling, General and Administration (“SG&A”) expenses include sales, marketing, general and administration costs (“G&A”), stock-based compensation, and depreciation and amortization expenses on G&A fixed assets. A breakdown of SG&A expenses into these components is presented below:

SG&A expenses for the three months ended June 30, 2017, was $2.3 million compared to $2.8 million in the same period in 2016 ($0.5 million decrease) or an 18% reduction. SG&A expenses excluding stock based compensation and amortization expenses (non-cash items) decreased by $0.4 million to $1.8 million for the three months ended June 30, 2017 ($2.2 million for the three months ended June 30, 2016). The main reductions were in salary and wages ($0.1 million) and (2) professional fees ($0.2 million). Stock-based compensation was $0.2 million for the three months ended June 30, 2017, compared to $0.3 million in the comparable period in 2016. The number of common shares available for issue under the stock compensation plan is 10% of the issued and outstanding common shares. During the quarter, compensation from vesting stock-based compensation awards was recognized, due to previously granted options and restricted shares. SG&A-related depreciation and amortization expenses for the three months ended June 30, 2017, were $0.4 million compared with $0.4 million for the same quarter of 2016. SG&A expenses for the first six months ended June 30, 2017, was $4.7 million compared to $6.0 million in the same period in 2016 or a 21% reduction. SG&A expenses excluding stock based compensation and amortization expenses (non-cash items) decreased by $1.0 million to $3.6 million for the six months ended June 30, 2017 ($4.6 million six months ended June 30, 2016). The main reductions were in (1) salary and wages ($0.3 million), (2) professional fees ($0.4 million) and (3) office expenses ($0.2 million). Stock-based compensation was $0.3 million for the six months ended June 30, 2017, compared with $0.5 million in the same quarter of 2016. The number of common shares available for issue under the stock compensation plan is 10% of the issued and outstanding common shares. During the period, compensation from vesting stock-based compensation awards was recognized, due to previously granted options and restricted shares. SG&A-related depreciation and amortization expenses for the six months ended June 30, 2017, were $0.8 million compared with $0.8 million for the same period of 2016.

Other Expenses

Other expenses for the three months ended June 30, 2017, was $2.2 million, a $1.0 million increase compared to $1.2 million for the same period in 2016. The increase in other expenses for the second quarter of 2017 of $1.0 million is attributable to (1) a decrease in other income ($1.1 million) and (2) an increase in interest expenses ($0.3 million), which were offset by (3) an increase in foreign exchange gains ($0.2 million) and (4) a recovery against inventory impairments ($0.2 million). Other expenses for the six months ended June 30, 2017, was $4.9 million, a $2.4 million increase compared to $2.5 million for the same period in 2016. The increase in other expenses for the six months ended June 30, 2017, of $2.4 million is attributable to (1) a decrease in other income ($1.0 million), (2) an increase in interest expenses ($0.3 million), (3) a decrease in foreign exchange gains ($0.8 million) and (4) a reduction in recoveries from bad debt expenses ($0.5 million), which were offset by (5) a recovery against inventory impairments ($0.2 million).

Other expenses for the three months ended June 30, 2017, was $2.2 million, a $1.0 million increase compared to $1.2 million for the same period in 2016. The increase in other expenses for the second quarter of 2017 of $1.0 million is attributable to (1) a decrease in other income ($1.1 million) and (2) an increase in interest expenses ($0.3 million), which were offset by (3) an increase in foreign exchange gains ($0.2 million) and (4) a recovery against inventory impairments ($0.2 million). Other expenses for the six months ended June 30, 2017, was $4.9 million, a $2.4 million increase compared to $2.5 million for the same period in 2016. The increase in other expenses for the six months ended June 30, 2017, of $2.4 million is attributable to (1) a decrease in other income ($1.0 million), (2) an increase in interest expenses ($0.3 million), (3) a decrease in foreign exchange gains ($0.8 million) and (4) a reduction in recoveries from bad debt expenses ($0.5 million), which were offset by (5) a recovery against inventory impairments ($0.2 million).

Net Loss

For the three months ended June 30, 2017, the Company had a net loss of $3.9 million, a decrease of $0.1 million or a 4% improvement over the comparable period in 2016 ($4.0 million loss). The $0.1 million decrease in net loss was driven by (1) an increase in gross profit ($0.6 million), (2) a decrease in SG&A expenses ($0.5 million) and (3) $0.1 million of net loss attributable to the non-controlling interest, which were offset by (4) an increase in other expenses ($1.0 million). For the six months ended June 30, 2017, the Company had a net loss of $8.3 million, a decrease of $0.1 million or a 1% improvement over the comparable period in 2016 ($8.4 million loss). The $0.1 million decrease in net loss was driven by (1) an increase in gross profit ($1.1 million), (2) a decrease in SG&A expenses ($1.3 million) and (3) $0.1 million of net loss attributable to the non-controlling interest, which were offset by (4) an increase in other expenses ($2.4 million).

Quarterly Basic and Diluted Loss per Share

The basic loss and diluted loss per share from operations was $0.10 for the three months ended June 30, 2017, compared with a basic and diluted net loss of $0.11 for the same period in 2016. The basic loss and diluted loss per share from operations was $0.22 for the six months ended June 30, 2017, compared with a basic and diluted net loss of $0.22 for the same period in 2016

Liquidity and Capital Resources

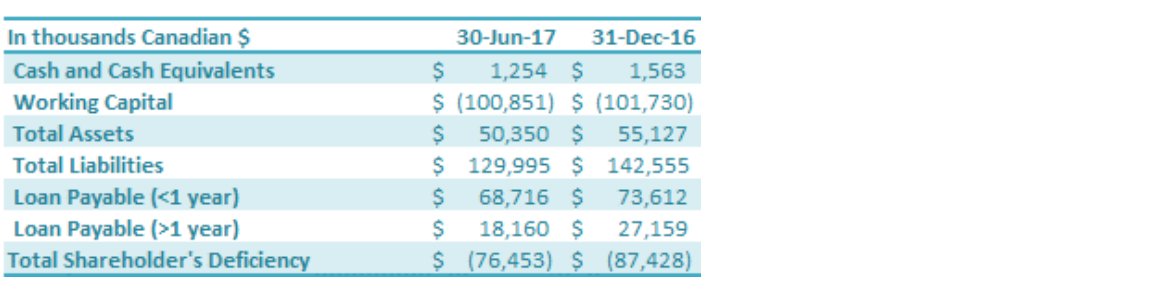

The Company continues to progress with the following measures to manage cash flow of the Company: paying down short-term loans, reducing accounts payable, negotiating with creditors for extended payment terms, working closely with the banks to restructure its loans, arranging financing with its Directors and other related parties, and reducing operating expenditures including general and administrative expenses and production-related expenses. Total loans payable (both short-term and long-term) is $86.8 million as of June 30, 2017, a decrease of $13.9 million compared to the total loans payable as at December 31, 2016 ($100.8 million). The decrease in loans was driven by the conversion of a portion of the related party debt into equity in one of GLG’s China subsidiaries, which was approved at the May 29, 2017, GLG Special Shareholders Meeting. The debt restructuring reduced short-term loans by $5.1 million and long-term loans by $10.8 million these reductions were partially offset by additional interest accrued over the period. The Company has worked with its Chinese banks on restructuring its Chinese debt. In 2015, the Construction Bank of China successfully transferred GLG’s debt to China Cinda Assets Management Co. and the Agricultural Bank of China successfully transferred GLG’s debt to China Hua Rong Assets Management Co., each of which is a state-owned capital management company (“SOCMC”). Prior to the Company’s Q2 2017 debt restructuring (see the Related Party Debt Conversion section), as of March 31, 2017, the total of all China bank loans transferred to SOCMCs accounted for approximately 74% of the Company’s outstanding Chinese debt. The nature of the business of these SOCMCs differs from banks, in that they take a long-term outlook on management of debt. For example, instead of simply requiring loan principal and interest payments, the SOCMCs aim to manage debts with greater flexibility, such as longterm loan terms, debt for equity arrangements, flexible debt retirement, and other long-term instruments. This debt is held at the Chinese subsidiary level, and any such potential arrangements would therefore be done at that level rather than at the corporate level. These SOCMCs could also be a source of possible future capital. The Company is working further with the Chinese banks and SOCMCs on restructuring its debt. The Corporate and Sales Developments section above describes a two-phase debt restructure plan. The first phase involved the conversion of related party debt into equity into one of the Company’s subsidiaries. The second phase is expected to involve the conversion of bank/SOCMC debt into equity in that same subsidiary. Ultimately, this two-phase plan is designed to eliminate approximately $100 million in debt and accrued interest.

Gross Profit Before Capacity Charges

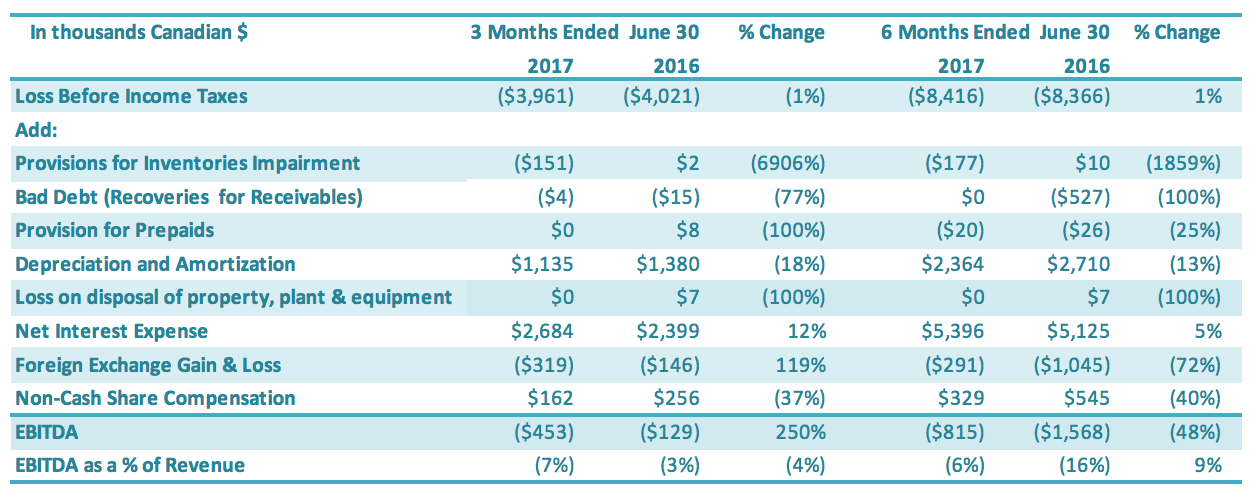

This non-GAAP financial measure shows the gross profit (loss) before the impact of idle capacity charges are reflected on the gross profit margin. GLG had only 50% of its production facilities in operation for the first six months of 2017 and idle capacity charges have a material impact on the gross profit (loss) line in the financial statements. Gross profit before capacity charges for the three months ended June 30, 2017, was $1.2 million or 18% of second quarter revenues compared to $0.9 million or 20% of second quarter revenues in 2016. Gross profit before capacity charges for the six months ended June 30, 2017, was $2.2 million or 18% of six-month revenues compared to $1.6 million or 17% of six-month revenues in 2016. Earnings Before Interest Taxes and Depreciation (“EBITDA”) and EBITDA Margin

EBITDA for the three months ended June 30, 2017, was negative $0.5 million or negative 7% of revenues, compared to negative $0.1 million or negative 3% of revenues for the same period in 2016. The 2016 EBITDA margin was impacted by the one-time increase of $1.0 million in other income received in the second quarter of 2016. Removing this impact on Q2 2016 would have resulted in EBITDA of negative $1.1 million and EBITDA margin of negative 28% compared to negative $0.5 million EBITDA and negative 7% EBITDA margin for the second quarter of 2017 ($0.6 million improvement). This improved Q2 2017 EBITDA margin is attributable to the higher gross margin achieved in the second quarter 2017 ($0.6 million) compared to the second quarter 2016 ($0.0 million) and the reduction in non-cash G&A expenses achieved in the second quarter of 2017 compared to the same period in 2016 ($0.4 million reduction). EBITDA for the six months ended June 30, 2017, was negative $0.8 million or negative 6% of revenues, compared to negative $1.6 million or negative 16% of revenues for the same period in 2016. The 2016 EBITDA margin was impacted by the one-time increase of $1.0 million in other income received in the second quarter of 2016. Removing this impact on the first six months of 2016 would have resulted in EBITDA of negative $2.6 million and EBITDA margin of negative 26% compared to negative $0.8 million EBITDA and negative 6% EBITDA margin for the six months ended June 30, 2017 ($1.8 million improvement). This improved 2017 EBITDA margin is attributable to the higher gross margin achieved in the first six months of 2017 ($1.1 million) compared to the same period in 2016 ($0.1 million) and the reduction in non-cash G&A expenses achieved in the first six months of 2017 compared to the same period in 2016 ($1.1 million reduction). Additional Information Additional information relating to the Company, including our Annual Information Form, is available on SEDAR (www.sedar.com). Additional information relating to the Company’s related party debt conversion transaction, as described in the Company’s Management Proxy Circular, is available on SEDAR (www.sedar.com). Additional information relating to the Company is also available on our website (www.glglifetech.com).

For further information, please contact:

Simon Springett, Investor Relations

Phone: +1 (604) 285-2602 ext. 101Fax: +1 (604) 285-2606

Email: [email protected]

About GLG Life Tech Corporation

GLG Life Tech Corporation is a global leader in the supply of high-purity zero calorie natural sweeteners including stevia and monk fruit extracts used in food, beverages, and dietary supplements. GLG’s vertically integrated operations, which incorporate our Fairness to Farmers program and emphasize sustainability throughout, cover each step in the stevia and monk fruit supply chains including non-GMO seed and seedling breeding, natural propagation, growth and harvest, proprietary extraction and refining, marketing and distribution of the finished products. Additionally, to further meet the varied needs of the food and beverage and supplement industries, GLG’s Naturals+ product line enables it to supply a host of complementary ingredients reliably sourced through its supplier network in China. For further information, please visit www.glglifetech.com.

Forward-looking statements:

This press release may contain certain information that may constitute “forward-looking statements” and “forward looking information” (collectively, “forward-looking statements”) within the meaning of applicable securities laws. Often, but not always, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes” or variations of such words and phrases or words and phrases that state or indicate that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved.

While the Company has based these forward-looking statements on its current expectations about future events, the statements are not guarantees of the Company’s future performance and are subject to risks, uncertainties, assumptions and other factors that could cause actual results to differ materially from future results expressed or implied by such forward-looking statements. Such factors include amongst others the effects of general economic conditions, consumer demand for our products and new orders from our customers and distributors, changing foreign exchange rates and actions by government authorities, uncertainties associated with legal proceedings and negotiations, industry supply levels, competitive pricing pressures and misjudgments in the course of preparing forward-looking statements. Specific reference is made to the risks set forth under the heading “Risk Factors” in the Company’s Annual Information Form published March 31, 2018. In light of these factors, the forward-looking events discussed in this press release might not occur.

Further, although the Company has attempted to identify factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

As there can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements, readers should not place undue reliance on forward-looking statements.

Leave a Reply